The Central Provident Fund (CPF) serves as Singapore’s essential savings mechanism, ensuring financial security for retirement, housing, and healthcare. As of January 1, 2025, significant revisions to CPF contribution rates and wage ceilings will come into effect, necessitating adjustments for both employers and employees. These changes are designed to better align with current economic conditions and to reinforce the CPF scheme as a vital support system, especially for older workers.

Revised Contribution Rates for 2025

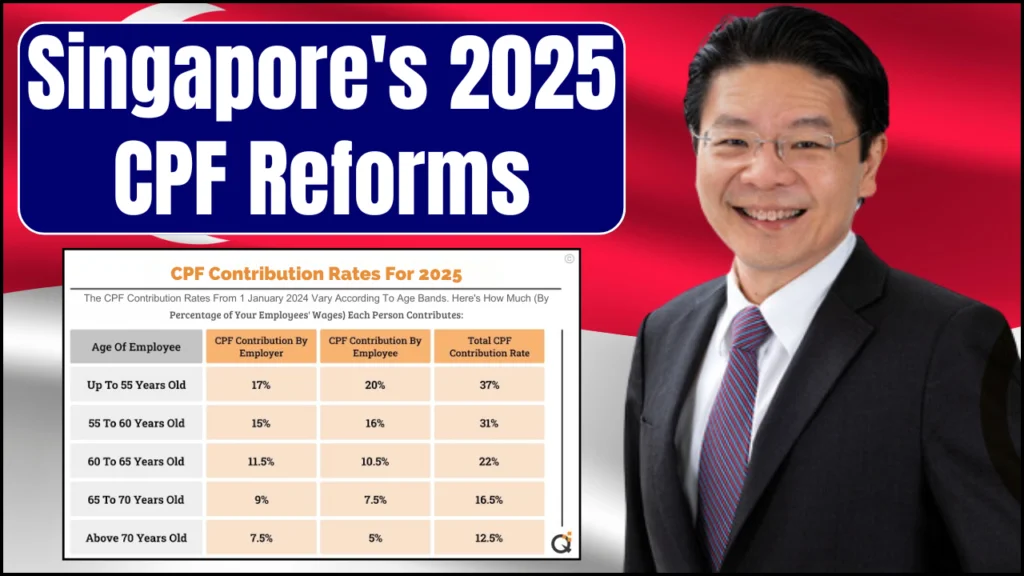

Under the new guidelines, CPF contribution rates have been updated with a particular focus on enhancing the retirement savings for employees aged between 55 and 65. The revised structure is segmented by age group, ensuring that contributions remain both fair and sustainable over the long term. The updated rates are detailed below:

- For employees aged 55 and below: Employers will contribute 17% of the employee’s wage, while the employee’s contribution is set at 20%. In total, this age group will contribute 37% of their wage to CPF.

- For employees above 55 up to 60: The employer’s contribution drops slightly to 15.5%, with employees contributing 17%, resulting in a total contribution rate of 32.5%.

- For employees over 60 to 65: The employer’s share is further reduced to 12%, and the employee contributes 11.5%, bringing the combined rate to 23.5%.

- For employees aged above 65 up to 70: The contribution rates continue to decline with employers contributing 9% and employees contributing 7.5%, which sums up to 16.5%.

- For employees above 70: The lowest contribution rates apply, with employers paying 7.5% and employees 5%, totaling a 12.5% contribution.

These adjustments ensure that the CPF remains a robust support system while reflecting the changing financial needs as individuals age. The intention is to provide increased security for older workers by reducing the financial burden on them, while still encouraging substantial savings for retirement.

Navigating the New Retirement Era, Singapore’s Updated Age and Re-Employment Policies

S$600 Singapore Cost of Living Payment, Payment Details and How To Check If You Qualify

S$840 – S$900 Monthly Payout in Singapore, Eligibility, Dates & Benefits

Singapore’s 2025 Assurance Package, Eligibility, Deadline, and Benefits

Allocation of CPF Contributions

CPF contributions are distributed across three main accounts, each serving a distinct purpose:

- Ordinary Account (OA): Funds in this account can be used for a variety of purposes such as housing, insurance, investments, and education. It plays a crucial role in helping Singaporeans achieve home ownership and further their educational opportunities.

- Special Account (SA): This account is earmarked specifically for old-age savings and is intended to fund retirement-related investments. The SA’s focus is on ensuring that individuals have a dedicated pool of funds for their golden years.

- MediSave Account (MA): Designed to cover hospitalization expenses and approved medical insurance, this account ensures that Singaporeans have sufficient funds set aside for healthcare needs.

When an individual reaches the age of 55, the CPF structure undergoes a significant change where the OA and SA are consolidated into a single Retirement Account (RA). This account is then used to provide retirement payouts, ensuring a smooth transition into retirement while securing a steady income stream.

Changes to CPF Wage Ceilings

One of the notable changes in the 2025 update is the adjustment of CPF wage ceilings. The Ordinary Wage (OW) ceiling is being progressively increased, with a planned gradual increase from S$6,000 to S$8,000 by 2026. For 2025 specifically, the OW ceiling will be raised to S$7,400, up from S$6,800 in 2024. This adjustment reflects Singapore’s commitment to ensuring that CPF contributions keep pace with rising incomes and inflation, thereby maintaining the adequacy of retirement savings.

Implications for Employers and Employees

The changes to CPF contribution rates and wage ceilings have significant implications for both employers and employees. Employers are required to update their payroll systems to accommodate the revised rates, ensuring that deductions and contributions are correctly calculated. This adjustment might involve software updates or additional training for payroll personnel to ensure compliance with the new regulations.

For employees, the changes mean that careful financial planning becomes even more critical. With varying contribution rates based on age, employees need to be aware of how these adjustments will impact their overall CPF savings and retirement planning. The CPF Board offers various calculators and online tools designed to help individuals understand and manage these changes effectively.

Moreover, for employees earning between $500 and $750 monthly, the CPF contribution adjustments are being phased in gradually, ensuring that the changes do not impose an abrupt financial strain on lower-income workers. This phased approach is a thoughtful measure aimed at balancing fiscal responsibility with social welfare.

Broader Objectives

The CPF revisions set for 2025 are part of a broader strategy to enhance the retirement security of Singaporeans, especially as the population ages. By adjusting the contribution rates, particularly for older workers, the CPF scheme aims to provide more meaningful retirement payouts while reducing the immediate financial burden on those closer to retirement age. The incremental increases in the CPF wage ceiling also signal a commitment to aligning retirement savings with the evolving economic landscape.

For employers, these changes represent a need to stay current with regulatory updates and ensure that payroll systems are accurately configured to comply with the new rates. Employees, on the other hand, must adapt their financial planning strategies to make the most of their CPF contributions. Staying informed about these changes is crucial for maximizing the benefits of the CPF scheme and ensuring long-term financial stability.

Final Thoughts

The 2025 CPF updates are a clear indicator of Singapore’s proactive approach to safeguarding its citizens’ futures. By revising the contribution rates and wage ceilings, the government is not only addressing current economic realities but also laying a solid foundation for a more secure retirement for all. Both employers and employees are encouraged to leverage the tools provided by the CPF Board to navigate these changes effectively and to plan strategically for a financially secure retirement.